Last October, 74 year old Linda sat at her kitchen table in San Diego staring at a property tax bill that had increased by 20% since 2021. You likely feel that same tightening in your chest when the mail arrives, knowing that a fixed income doesn’t always stretch to meet California’s rising demands. It’s frustrating to think that the home you’ve owned for decades could be at risk simply because of a tax assessment. This is why the property tax postponement for seniors California program is such a critical tool for homeowners who want to stay put.

We understand that you want to protect your legacy without sacrificing your daily quality of life. This guide will show you exactly how to defer those annual payments to ensure your financial security and help you age in place. We’ll cover the latest 2026 household income limits, explain the 5% interest rate applied by the State Controller’s Office, and outline the long term impact on your heirs. You’ll finish this article with a clear, step by step path to securing your home and your peace of mind before the next filing deadline.

Key Takeaways

- Learn how this state-funded loan program allows you to defer current-year property taxes to preserve your cash flow and financial security.

- Identify the specific age and residency requirements you must meet to qualify for the 2026 program and age in place with confidence.

- Follow a clear, step-by-step timeline to secure property tax postponement for seniors California by gathering the necessary documentation for the State Controller’s Office.

- Understand the 7% interest rate and the specific life events that trigger the end of your tax deferment and require repayment.

- Evaluate whether deferring your taxes or transitioning to a more manageable home with a Senior Real Estate Specialist is the best strategic move for your future.

What is the California Property Tax Postponement (PTP) Program?

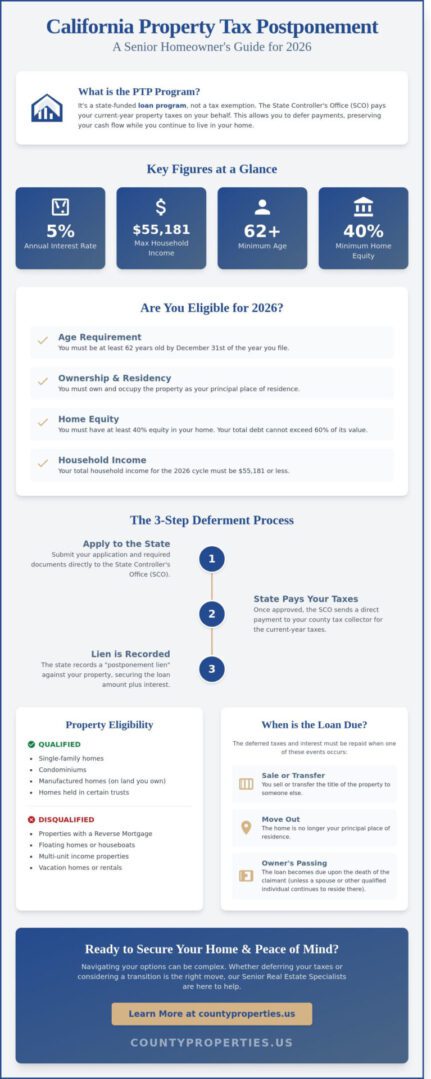

Our team at County Properties understands that staying in your home is a top priority as you age. The California Property Tax Postponement (PTP) program acts as a financial safety net for eligible homeowners who need more breathing room in their monthly budgets. This state-funded loan allows you to defer payment of your current-year property taxes on your primary residence. Since California’s property tax system is governed by complex rules like Proposition 13, many seniors find themselves “house rich but cash poor” as home values rise while fixed incomes remain static.

It is vital to distinguish this program from property tax exemptions or “circuit breaker” programs. Exemptions permanently reduce the amount of tax you owe. PTP is a deferral, meaning you aren’t getting a discount on the tax itself. Instead, the state pays your bill now, and you repay the state at a later date. The State Controller’s Office (SCO) manages this program rather than local county assessors. This centralized management ensures that eligibility requirements stay uniform across all 58 counties, providing a consistent experience for every applicant.

How the Deferment Works

When you qualify for property tax postponement for seniors California, the SCO sends a direct payment to your specific county tax collector. In exchange for this payment, the state records a “postponement lien” against your property. This legal document secures the state’s interest, much like a traditional mortgage. You should view this as a low-interest loan rather than a grant. As of 2024, the interest rate for the program is set at 5% per year. You don’t make monthly payments toward the balance. The loan only becomes due when you sell the property, move, or pass away.

The History and Stability of PTP in 2026

The program has a resilient history that proves its reliability. California suspended PTP in 2009 during the Great Recession due to state budget shortages, but the legislature reinstated it in 2016 with more robust oversight. In 2026, funding levels remain stable, making it a dependable resource for long-term financial planning. Homeowners in Southern California increasingly utilize this resource to manage the high cost of living without sacrificing their home equity. Because the program is backed by state legislation and specific funding allocations, it offers a level of security that private equity-release products often lack. Utilizing property tax postponement for seniors California helps you maintain your independence while keeping your financial legacy intact.

Eligibility Requirements for Seniors in 2026

The state of California maintains strict criteria to ensure this financial safety net reaches those who need it most. To qualify for property tax postponement for seniors California in 2026, you must meet four primary benchmarks. First, you must be at least 62 years old by December 31 of the year you file your claim. This age requirement is firm. Second, you must own and occupy the property as your principal place of residence. This means the home isn’t a vacation property or a rental; it’s where you live most of the year.

Equity is the third major hurdle. You must have at least 40% equity in your home. To calculate this, the state compares your property’s current market value against all outstanding debt, including your primary mortgage and any secondary liens. If your total debt exceeds 60% of the home’s value, you won’t qualify. Finally, your total household income for the 2026 cycle must be $55,181 or less. This income cap is adjusted annually, so it’s vital to check the latest figures from the Property Tax Postponement (PTP) Program before you start your paperwork.

Qualified Property Types

The program covers most traditional housing, including single-family homes and condominiums. Certain manufactured homes also qualify if they are permanently situated on land you own. However, there are clear exclusions. You cannot use this program for floating homes, houseboats, or multi-unit income properties where you don’t occupy the entire structure. If your home is held in a trust or you hold a life estate, you may still be eligible. You’ll just need to provide specific trust documentation to prove you’re the primary beneficiary with the right to occupy the home.

The “No Reverse Mortgage” Rule

Having a reverse mortgage is one of the most common reasons seniors are disqualified from the PTP program. This happens because the state requires a specific lien priority to protect its interest. Since a reverse mortgage balance grows every month, it can eventually consume the equity the state needs to ensure the deferred taxes are eventually repaid. This creates a conflict between the private lender and the State Controller’s Office.

If you have a Home Equity Line of Credit (HELOC), you might also face challenges. The state often views the entire credit limit of a HELOC as debt, even if your current balance is zero. This can push your debt-to-equity ratio above the 60% limit. If you’re unsure how your current loans impact your eligibility, speaking with an experienced real estate guide can provide the clarity you need to move forward with confidence. We’ve spent 36 years helping homeowners manage these complex transitions, ensuring you have the right information to protect your financial security.

The Application Process and 2025-2026 Timeline

Securing your financial future starts with a clear plan and the right paperwork. To begin, you must obtain the official application package directly from the State Controller’s Office. You can download these forms from their website or request a physical copy by mail. The California Property Tax Postponement Program provides a vital safety net, but you must follow their specific protocol to qualify. Once you have the forms, your next task is gathering proof of eligibility. You’ll need your most recent federal and state income tax returns along with your current property tax bill. If you don’t file income tax returns, you’ll need to provide alternative documentation like Social Security benefit statements or 1099 forms to verify your household income.

Timing is everything. The state allocates a specific budget for this program each year, and funds are distributed until they’re gone. You should submit your completed claim as soon as the filing window opens to ensure you’re at the front of the line. Because the program uses a first-come, first-served funding model, early applicants have a much higher success rate than those who wait. After you mail your application, monitoring your status is the final piece of the puzzle. The state typically takes several weeks to review your file. You’ll receive a notification letter once they reach a decision. If approved, the state pays your property taxes directly to the county, and a lien is placed on your property to secure the loan.

Key Dates for the 2026 Tax Year

Staying ahead of the calendar ensures you don’t miss out on property tax postponement for seniors California. For the 2025-2026 cycle, mark these specific dates on your calendar to remain compliant with state requirements:

- September 2025: The State Controller’s Office releases the new application forms for the upcoming cycle.

- October 1, 2025: The official filing period begins. This is the earliest date you can submit your claim.

- February 10, 2026: This is the final hard deadline for application submission. Any claims postmarked after this date will be rejected.

Common Application Mistakes to Avoid

Errors often lead to delays or outright denials of your benefits. One frequent issue is incomplete income reporting. You must include the total household income for every person living in the home, not just the primary applicant. Another mistake involves missing proof of age or disability status. Ensure you include a clear copy of your California ID or valid medical documentation if applying based on a disability. Finally, remember that submitting after the program funding is exhausted will result in a denial, even if you meet all other criteria. Applying for property tax postponement for seniors California requires precision, so double-check every attachment before sealing the envelope.

Repayment: When and How the Deferment Ends

While the property tax postponement for seniors California program provides immediate financial breathing room, it functions as a loan from the state. It’s essential to understand that this isn’t a waiver of your tax obligations. The State Controller’s Office pays your property taxes directly to the county, and in exchange, they place a lien on your home to secure that debt. For the 2026 tax year, the state applies a 7% annual simple interest rate to the postponed amount. Because this interest is simple rather than compounded, the balance grows more slowly than a typical credit card or bank loan, but it still reduces your home equity over time.

You don’t have to wait for a specific event to start paying back the funds. Many seniors choose to make voluntary partial payments when they have extra cash from a tax refund or an inheritance. Making early payments helps keep the total interest lower and preserves more of the home’s value for your heirs. If you decide to pay the full balance early, the state will release the lien, clearing your title of this specific debt.

Mandatory Repayment Triggers

The state requires full repayment of the principal and interest when certain life changes occur. The most common trigger is when the home is no longer your principal residence. If you move into an assisted living facility or a different home, the deferred taxes become due immediately. Similarly, if you sell the property or convey the title to someone else, the debt must be settled. In the event of the claimant’s death, the total amount becomes due unless there is a surviving spouse who also meets the program requirements and continues to live in the home.

Calculating the Long-Term Cost

To visualize the impact, imagine a homeowner who postpones $5,000 in property taxes annually for five years. By the end of year five, the principal debt is $25,000. At a 7% simple interest rate, the total interest accrued would be approximately $5,250, bringing the total lien to $30,250. While this may seem like a large sum, housing market trends in Southern California often show property appreciation that significantly outpaces this debt growth. During a standard home sale, the escrow company pays the state directly from the proceeds to satisfy the lien before the remaining equity is distributed to the seller.

If you’re concerned about how a tax lien might affect your estate planning or your ability to sell in the future, our team can help you evaluate your options. Contact our expert advisors for personalized guidance on managing your property equity.

Strategic Alternatives: Is Postponement or Selling Right for You?

Deciding between the property tax postponement for seniors California program and a fresh start requires a clear look at your long-term goals. While the state program offers immediate relief, it’s essentially a lien on your property. For some, this is a perfect bridge. For others, it’s a temporary fix for a larger financial challenge. You have to weigh the comfort of your current home against the potential freedom of a more manageable lifestyle.

When Postponement is the Smart Move

The program works best if you have high home equity but face temporary cash flow issues. If you’ve lived in your San Diego or Riverside neighborhood for decades and want to “age in place,” postponement keeps you in familiar surroundings. It’s also a viable strategy if your heirs plan to keep the house. Since the state’s lien is settled when the home is eventually sold or transferred, heirs can pay off the balance later, allowing you to live comfortably now without the stress of a move.

When Selling and Moving Makes More Sense

Sometimes, the costs of homeownership go beyond just taxes. If annual maintenance, rising insurance premiums, and utility bills are draining your savings, a tax delay won’t solve the core problem. You might find better value by selling a home in SoCal to unlock significant equity. This capital can fund a transition to a modern, low-maintenance condo or a high-quality assisted living facility. As we look toward the 2026 market, timing your transition can help you maximize your retirement nest egg before market shifts occur.

County Properties specializes in these delicate transitions. Working with a Senior Real Estate Specialist (SRES) provides more than just a listing agent. Our team offers “turn-key” solutions that handle everything from decluttering to financial guidance. Arnie Levine’s 36 years of experience ensures you aren’t just making a transaction; you’re securing your future. We help you weigh the property tax postponement for seniors California option against the benefits of downsizing.

- Downsizing: Reduces monthly overhead and physical labor.

- Equity Access: Provides liquid cash for medical needs or travel.

- Simplified Living: Smaller footprints often mean fewer safety hazards for seniors.

- Expert Guidance: Our team coordinates the entire move, so you don’t have to.

Whether you choose to stay or start a new chapter, the goal is financial peace of mind. If the burden of taxes and upkeep has become too much, it’s time to look at the numbers. We’re here to provide the data and support you need to make the right choice for your family.

Securing Your Financial Future in 2026 and Beyond

The California Property Tax Postponement (PTP) program remains a vital safety net for homeowners aged 62 and older. As you navigate the 2025-2026 application cycle, remember that eligibility requires a household income of $53,730 or less and at least 40% equity in your primary residence. While this deferment provides immediate relief, it’s essential to understand that the state places a lien on your property. This means the debt must be settled when you sell the home or if the title transfers.

Deciding between property tax postponement for seniors California or exploring a strategic sale requires a clear look at your long-term goals. You don’t have to make these complex financial decisions alone. Our team brings over 36 years of Southern California real estate experience to the table, combined with specialized SRES® (Senior Real Estate Specialist) training. We use a collaborative team approach to ensure your financial security is prioritized and your transition is seamless.

Speak with our Senior Real Estate Specialists for personalized guidance. We’re here to help you move forward with confidence and peace of mind.

Frequently Asked Questions

Is the property tax postponement program the same as a tax exemption?

No, the PTP program is a deferment loan rather than a permanent tax reduction. While a tax exemption like the $7,000 California Homeowners’ Exemption reduces your bill forever, PTP simply delays payment. The state pays your taxes now and attaches a lien to your home. You’ll eventually pay back the principal plus 7% interest when you sell the property or move.

What is the maximum income to qualify for property tax postponement in California for 2026?

The California State Controller hasn’t released the exact 2026 figure yet, but the current 2024-2025 income limit is $51,762. This threshold usually adjusts every year based on inflation and cost of living metrics. You should check the official SCO website in late 2025 for the updated number. Eligibility depends on your total household income from the previous calendar year, including Social Security and pensions.

Can I qualify for PTP if I have a reverse mortgage on my San Diego home?

You can’t qualify for property tax postponement for seniors California if you already have a reverse mortgage on your San Diego home. The state requires a specific lien priority to secure the loan. Because reverse mortgages take up that primary position, the State Controller’s Office won’t approve the application. It’s vital to review your current loan documents before starting the process.

Does the state take ownership of my house if I postpone my taxes?

No, you keep full ownership and the deed to your home while participating in the program. The state simply files a “Notice of Lien” with the county recorder to secure their interest. This works similarly to a standard mortgage or a home equity line of credit. You’re free to live in the home as long as it remains your primary residence and you maintain the property.

What happens to the postponed taxes when I pass away?

The postponed taxes and accrued interest become due immediately upon your passing. Your heirs or the executor of your estate typically have 6 months to settle the balance with the State Controller. If they can’t pay the debt through other assets, they might need to sell the home to clear the lien. It’s a good idea to discuss this with your family during your estate planning.

Can I postpone my taxes if I am under 62 but have a disability?

Yes, you can qualify if you’re under 62 and meet the state’s disability requirements. The program specifically includes individuals who are blind or have a permanent disability as defined by the Social Security Act. You’ll need to provide medical documentation or a rewards letter to prove your status. This ensures younger residents facing financial hardship due to health issues can stay in their homes safely.

How does the 7% interest rate compare to other senior financial products?

The 7% simple interest rate is often lower than unsecured debt but higher than some traditional mortgages. For example, many credit cards carry interest rates exceeding 21%, and current HELOC rates often hover around 9%. Since this is simple interest rather than compound interest, the balance grows slower than a typical bank loan. It’s a specialized tool for preserving your monthly cash flow during retirement.

Is there a limit to how many years I can postpone my property taxes?

There isn’t a specific limit on the number of years you can use property tax postponement for seniors California. You’re allowed to apply every year as long as you continue to meet the income requirements and maintain at least 40% equity in your home. Each year requires a fresh application to the State Controller’s Office between October 1 and February 10 to ensure your taxes are covered.