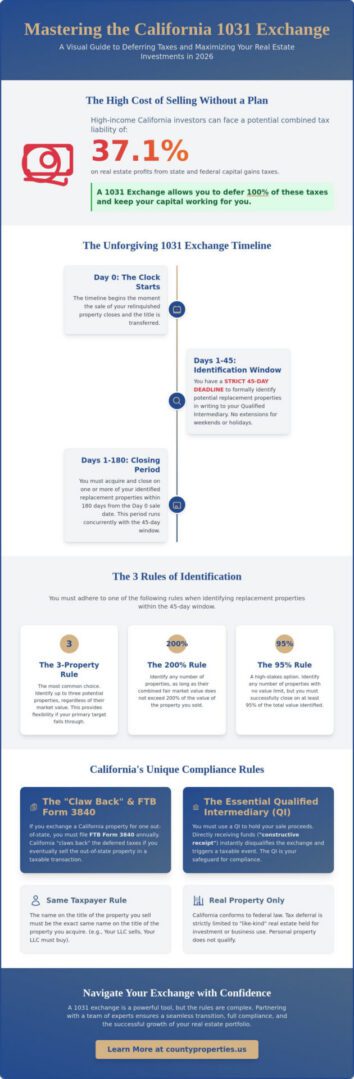

Did you know that high-income investors in the Golden State could face a combined tax hit of 37.1% on their real estate profits this year? Between California’s 13.3% top income tax rate and federal obligations, selling an investment property without a plan often feels like watching your hard-earned equity evaporate. Mastering the 1031 exchange rules California 2026 is no longer just a savvy tax strategy; it’s a vital necessity for anyone looking to protect their financial legacy and keep their capital working.

We understand the pressure of the 45-day identification window, especially when quality replacement properties are hard to find in a competitive market. You’ve spent years building your portfolio. The last thing you want is a “claw back” tax notice from the Franchise Tax Board because of a simple filing error. This guide will help you navigate these complexities so you can defer 100% of your capital gains taxes and successfully transition into higher-performing assets. We’ll walk through mandatory FTB Form 3840 filings, the strict 180-day closing timeline, and the proactive strategies you need to ensure full compliance while your wealth grows.

Key Takeaways

- Understand the “Day Zero” rule to master the strict 45-day identification and 180-day closing deadlines that govern every successful exchange.

- Learn how the 1031 exchange rules California 2026 align with federal guidelines to help you defer capital gains and build long-term wealth.

- Discover the lifelong reporting requirements of the California “claw back” provision and how FTB Form 3840 tracks your equity across state lines.

- Identify strategic opportunities to transition from high-maintenance rentals into passive, high-performing assets in markets like San Diego.

- See how a collaborative team of professional allies ensures you avoid taxable “boot” and maintain full compliance with the Franchise Tax Board.

Understanding 1031 Exchange Rules in California for 2026

Mastering the 1031 exchange rules California 2026 starts with a simple premise. You are not “selling” a property; you are swapping your equity from one “relinquished” asset into a “replacement” asset of equal or greater value. This process relies on the concept of tax deferral, allowing you to keep 100% of your capital gains working within your portfolio rather than losing a significant portion to state and federal taxes. While many investors assume “like-kind” means swapping an apartment building for another apartment building, the definition is actually much broader. In the eyes of the tax authorities, almost any real property held for productive use in a trade, business, or for investment qualifies. You can transition from a high-maintenance single-family rental into a passive triple-net lease retail space or even raw land, provided the intent remains investment-focused.

Federal vs. California State Conformity

California’s tax code largely mirrors the federal Internal Revenue Code section 1031, but there are specific nuances you must respect. As of 2026, California law maintains its conformity date to the federal code as of January 1, 2025. This alignment is critical because it confirms that California strictly limits 1031 treatment to real property. Following the federal Tax Cuts and Jobs Act, personal property like equipment, vehicles, or even certain fixtures no longer qualifies for tax-deferred treatment in the Golden State.

You must also adhere to the “Same Taxpayer” rule to ensure a successful exchange. This means the individual or entity listed on the title of the relinquished property must be the exact same entity that takes title to the replacement property. Whether you hold your assets in a living trust, an LLC, or as an individual, consistency is the key to avoiding a rejected filing by the Franchise Tax Board (FTB).

The Role of the Qualified Intermediary (QI)

To maintain the integrity of your exchange, you can never personally touch the sale proceeds. If you receive even a moment of “constructive receipt” of the funds, the 1031 exchange rules California 2026 dictate that the transaction becomes a taxable sale. A Qualified Intermediary (QI) acts as your essential professional ally, holding the exchange funds in a secure, segregated account until the purchase of your replacement property is finalized.

Your QI does more than just hold money; they coordinate the complex logistics between the IRS and the FTB. When selecting a QI in Southern California, prioritize firms with institutional-grade security and deep experience in California-specific reporting. They ensure that all required documentation is filed correctly, protecting your equity from accidental exposure to the state’s aggressive tax collection efforts.

The Strict 1031 Timeline: 45 Days to Identify and 180 to Close

Success in a tax-deferred swap isn’t just about finding the right building; it’s about racing against a relentless clock. The 1031 exchange rules California 2026 are unforgiving regarding deadlines. Your journey starts on “Day Zero,” the date you officially transfer the title of your relinquished property to the buyer. From that moment, you have exactly 45 calendar days to identify potential replacement properties. It’s a common trap to assume that if the 45th day falls on a weekend or a legal holiday, you get an extension. You don’t. Missing this window by even a few minutes can disqualify the entire exchange, leaving you with an immediate tax bill on your equity.

The Three Rules of Identification

To stay compliant, you must follow one of three specific identification methods to notify your Qualified Intermediary of your intent:

- The 3-Property Rule: This is the most popular choice. It allows you to name up to three properties of any fair market value, giving you multiple options if your first choice falls through.

- The 200% Rule: You can identify any number of properties, provided their combined fair market value doesn’t exceed 200% of the property you sold.

- The 95% Rule: This is a high-stakes exception. You can identify any number of assets, but the exchange only works if you actually close on at least 95% of the total value identified.

Managing the 180-Day Closing Pressure

The remaining 135 days of your 180-day window are dedicated to closing the deal. This might sound like plenty of time, but financing hurdles, environmental inspections, and appraisal delays can eat into that buffer quickly. We recommend studying the latest Southern California housing market trends before you even list your current asset. By starting your search early, you reduce the “identification panic” that often leads investors to overpay for a mediocre asset just to save on taxes. Adhering to the 1031 exchange rules California 2026 requires you to have a backup plan for your backup plan.

If your search takes you beyond state lines, you must also prepare for California’s Unique ‘Claw Back’ Rule and FTB 3840, which tracks your deferred gain indefinitely. Our team provides expert Seller Representation to help you coordinate these moving parts with confidence, ensuring you meet every deadline without the stress of last-minute scrambles.

California’s Unique ‘Claw Back’ Rule and FTB 3840

Many investors believe that moving their equity out of the Golden State means leaving California’s tax reach behind. This is a costly misconception. Under the 1031 exchange rules California 2026, the Franchise Tax Board (FTB) maintains a very long memory through what is commonly known as the “claw back” provision. If you sell California real estate and reinvest the proceeds into a replacement property in a state like Florida, Texas, or Arizona, California doesn’t simply waive the tax. Instead, it tracks that deferred gain indefinitely. The state’s logic is simple: the appreciation happened while the asset was on California soil, so the state is entitled to its share of the tax whenever that gain is finally “recognized” in a taxable sale.

Reporting Like-Kind Exchanges to the FTB

To keep this deferral active, you must file FTB Form 3840, California Like-Kind Exchanges, for the year of the exchange and every single year thereafter. This form serves as an annual “check-in” with the state. It identifies the “California Sourced” gain, which is the specific amount of profit you deferred when you left the state. As of 2026, the FTB has significantly ramped up its enforcement. They now utilize an AI-driven system called Enterprise Data to Revenue (EDR2) to cross-reference federal filings with state records. If you fail to file Form 3840, the system may automatically trigger a notice of proposed assessment. This means the state assumes you sold the out-of-state property and will demand the deferred tax immediately at California’s standard income tax rates, which currently reach as high as 13.3%.

Strategic Considerations for Out-of-State Exchanges

Managing an out-of-state exchange requires a commitment to meticulous record-keeping that may span decades. You or your heirs must keep copies of the original closing statements and every Form 3840 filed over the 20 to 30 year reporting horizon. For many, the administrative burden is a small price to pay for the ability to transition equity into markets with higher yields or lower property taxes.

However, there is one way to truly settle the score with the claw back rule: the “swap til you drop” strategy. If you continue to exchange properties until your passing, your heirs receive a “step-up in basis” to the current fair market value. This effectively wipes out the deferred capital gains tax at both the federal and state levels. It’s a powerful legacy-building tool, but it requires a disciplined, long-term approach to portfolio management. We focus on helping you weigh these state-specific burdens against your long-term goals, ensuring your transition out of California is as seamless as your growth within it.

Strategies for Identifying High-Performing Replacement Properties

Successfully navigating the 1031 exchange rules California 2026 requires a shift from a defensive tax mindset to an offensive growth strategy. While the 45-day identification window feels short, it is your opportunity to upgrade your portfolio’s performance. Many savvy investors are currently focusing their equity on San Diego and the Inland Empire. These regions offer a unique balance of reliable demand and long-term appreciation potential, making them ideal targets for those swapping out of lower-growth areas. When you’re evaluating these opportunities, it’s vital to distinguish between “Assessed Value” and “Market Value.” Your 1031 math must be based on the fair market value of the replacement asset to ensure you fully reinvest your proceeds and avoid taxable boot.

If you’re tired of the “toilets, tenants, and trash” that come with traditional rentals, you might consider a Delaware Statutory Trust (DST). This allows for fractional ownership in institutional-grade properties, giving you a passive income stream without management headaches. It’s a professional way to stay compliant with 1031 exchange rules California 2026 while diversifying your risk across multiple assets or geographic locations.

Transitioning from Residential to Commercial

Moving equity from residential rentals into commercial real estate Southern California is a proven path toward a more stable retirement. Triple Net (NNN) leases are particularly attractive for 1031 investors because the tenant typically covers property taxes, insurance, and maintenance. This structure transforms a volatile real estate holding into a predictable, bond-like asset. However, you must understand the different risk profiles in 2026; industrial and medical office spaces often provide more resilience than traditional retail in the current economic environment.

Leveraging Local Expertise for Rapid Identification

The tight Southern California market can make finding a replacement property feel impossible within 45 days. This is where off-market listings become your greatest asset. Accessing properties before they hit the open market allows you to bypass bidding wars and secure your exchange with confidence. We always advise clients to include a “backup” property on their identification list to protect against a primary deal falling through at the last minute. A seasoned local agent streamlines the due diligence process and coordinates with your lender to ensure your 180-day close remains on track. If you’re ready to find your next high-performing asset, our team offers expert Buyer Representation to guide you through every step of the acquisition.

Partnering with a 1031 Expert for a Seamless Transition

Executing a successful tax-deferred swap is rarely a solo endeavor. It requires a synchronized effort between three key professionals: your real estate agent, your CPA, and your Qualified Intermediary. While the 1031 exchange rules California 2026 provide a clear roadmap, the logistical reality of managing deadlines and documentation can be overwhelming. County Properties acts as your central hub during this process. We coordinate the flow of information so your CPA has the exact data needed for tax filings and your QI remains in full compliance with the strict “constructive receipt” rules. This collaborative approach ensures that no detail is overlooked, protecting your equity from accidental taxation.

Our team specializes in managing the complex logistics of 1031 sales in the Southern California market. We don’t just list your property; we build a timeline that respects the 45-day identification window from the very start. By preparing your replacement strategy before your relinquished property even hits the market, we eliminate the panic that leads to poor investment choices. This proactive method is the hallmark of a seasoned professional ally who understands that your financial security is the top priority.

Senior Real Estate Transitions

For older investors, a 1031 exchange is often about more than just growth. It’s about lifestyle and legacy. Many of our clients are transitioning away from management-intensive residential units toward passive income properties that require less daily oversight. Working with a senior real estate specialist allows you to explore tailored solutions that maximize your current cash flow while preserving wealth for your heirs. Whether you are downsizing your portfolio or shifting equity into a NNN lease, we provide the empathetic, methodical support you need during these high-stakes life transitions.

Your Next Steps with County Properties

The path to a successful 2026 exchange begins with a clear understanding of your property’s current standing. We provide a comprehensive market analysis for your relinquished asset to ensure your “exchange value” is calculated accurately. Once we have a baseline, our team pre-screens potential replacement properties, often accessing off-market opportunities that give you a competitive edge in a tight market. This preparation is vital for meeting the 45-day rule with confidence.

If you’re ready to protect your capital gains and strategically grow your real estate portfolio, don’t leave the details to chance. Schedule a 1031 exchange consultation with Arnie Levine today to begin crafting your personalized transition plan. We’re here to act as your dependable guide, ensuring every step of your exchange is handled with professional mastery and care.

- Final Exchange Checklist:

- Select a reputable Qualified Intermediary before closing your sale.

- Confirm your replacement property meets the “Like-Kind” real property requirement.

- Formally identify your replacement assets within 45 days of your sale.

- Complete the acquisition of your new property within the 180-day window.

- Ensure your CPA is prepared to file Form 8824 and, if necessary, FTB Form 3840.

Secure Your Wealth and Legacy Through Strategic Tax Deferral

Mastering the 1031 exchange rules California 2026 is about more than just avoiding a heavy tax bill; it’s about making a commitment to your long-term financial growth and stability. You now understand the vital importance of the strict 45-day identification window and the persistent nature of the state’s “claw back” reporting requirements for out-of-state moves. By shifting from high-maintenance rentals to passive, high-performing assets, you aren’t just saving on taxes. You’re reclaiming your time and building a more resilient portfolio for the years ahead.

Success in these complex transitions requires a seasoned professional who understands the specific needs of Southern California investors. Led by Arnie Levine, a veteran with deep roots in the region, our team specializes in senior real estate transitions and collaborative portfolio management. We work side-by-side with your tax professionals and qualified intermediaries to ensure every deadline is met with precision and every filing remains fully compliant with the Franchise Tax Board.

Maximize your investment potential—let us guide your 2026 1031 exchange.

Your equity represents years of hard work and vision. We’re here to help you protect that legacy and move forward into your next investment chapter with total confidence and peace of mind.

Frequently Asked Questions

Can I do a 1031 exchange on my primary residence in California?

No, you cannot use a 1031 exchange for your primary residence. These tax-deferred swaps are strictly reserved for properties held for productive use in a trade, business, or for investment purposes. If you’re selling the home you live in, you should instead look into the Section 121 exclusion. This allows individuals to exclude up to $250,000, or $500,000 for married couples, of capital gains if specific residency requirements are met.

What happens if I identify a property within 45 days but the deal falls through?

You are limited to the properties you officially listed on your identification notice during the first 45 days. If those specific deals fail after the 45-day window has closed, you cannot identify new properties. This is why we strongly recommend identifying three solid options under the 3-Property Rule. Having a secondary and tertiary backup ensures your exchange stays viable even if your primary choice encounters unexpected inspection or financing hurdles.

Does California tax 1031 exchanges differently than the IRS?

California generally follows federal guidelines, but it’s vital to remember that the state treats capital gains as ordinary income rather than using preferential rates. Under the 1031 exchange rules California 2026, you must also navigate the “claw back” provision if you move equity out of state. While the IRS doesn’t track your property across state lines for life, the California Franchise Tax Board does. This makes annual reporting via Form 3840 a mandatory requirement for any out-of-state swap.

How much time do I have to complete a 1031 exchange if I sell on December 31st?

You have until the earlier of 180 days or the due date of your tax return for the year the relinquished property was sold. If you close your sale on December 31st, your 180-day window would technically end in late June. However, because your tax return is typically due April 15th, you must either complete the exchange by that date or file a formal extension for your tax return. Filing an extension is a common strategy to secure the full 180 days.

Can I buy a replacement property that costs less than my relinquished property?

Yes, you can buy a less expensive property, but you’ll likely face a tax liability. To defer 100% of your capital gains, you must purchase a replacement property of equal or greater value and reinvest all net proceeds from the sale. If the new property costs less, or if you have a smaller mortgage on the replacement asset, the difference is considered “boot.” The IRS and FTB will tax that specific portion as a recognized gain.

What is a “boot” in a 1031 exchange and how is it taxed?

Boot is any non-like-kind property or cash you receive as part of the exchange. This often happens if you don’t reinvest the full sale proceeds or if your new debt is lower than the debt on the property you sold. In California, boot is taxed as ordinary income at rates ranging from 1% to 13.3%. We focus on helping you structure your purchase to eliminate boot, ensuring your equity remains fully protected within your new investment.

Is a 1031 exchange worth it if I only have a small amount of equity?

It depends on whether your projected tax savings outweigh the costs of the exchange. You must factor in the fees for a Qualified Intermediary and the potential for higher closing costs on the replacement asset. However, even with modest equity, the power of compound growth shouldn’t be underestimated. Deferring a $40,000 tax bill today allows that money to generate rental income and appreciation for decades, which often justifies the initial administrative effort.

Can I use a 1031 exchange to buy property for a family member to live in?

You can only do this if the property is treated as a legitimate investment and the family member pays fair market rent. The IRS and FTB require that the property is held for business or investment use. If you allow a family member to live there rent-free or at a significant discount, the authorities may view it as personal use. This could disqualify the exchange and trigger an immediate tax bill on your deferred gains.